Your Mutual Fund App Tells You You're Down 12%. It Doesn't Tell You Whether That's a Problem.

A few years ago, a relative of mine walked into her bank to renew a fixed deposit. She walked out having signed a ULIP form.

She didn't realise it until she tried to access her money three years later. The bank RM had been helpful, friendly, and very well incentivised. Traditional insurance plans earn banks up to 65% of the first-year premium in commissions. A mutual fund earns them around 1% annually. Researchers estimate Indian investors lost close to ₹1.5 trillion from mis-sold insurance policies in a single decade. The products got slightly better. The information asymmetry didn't.

What if she'd had someone in her corner before that conversation?

The Data Decision Chasm

Fintech solved the transaction problem. Buying a mutual fund takes three minutes. Comparing FD rates, there's an aggregator for that. But the last mile remains stubbornly human: Should I renew this FD or deploy the money somewhere else? My portfolio is down 18%, is that the market or is something wrong?

For these questions, your options are an RM with a target, a Reddit thread, or that one friend, the CA in the family, the colleague who always seems to have thought this through, who asks the right questions and has nothing to sell you. Available approximately never.

PFM apps have gotten good at showing you information. But the gap between data and decision, that's where people freeze, or walk into a ULIP.

LLMs bring Intelligence, enable Agency

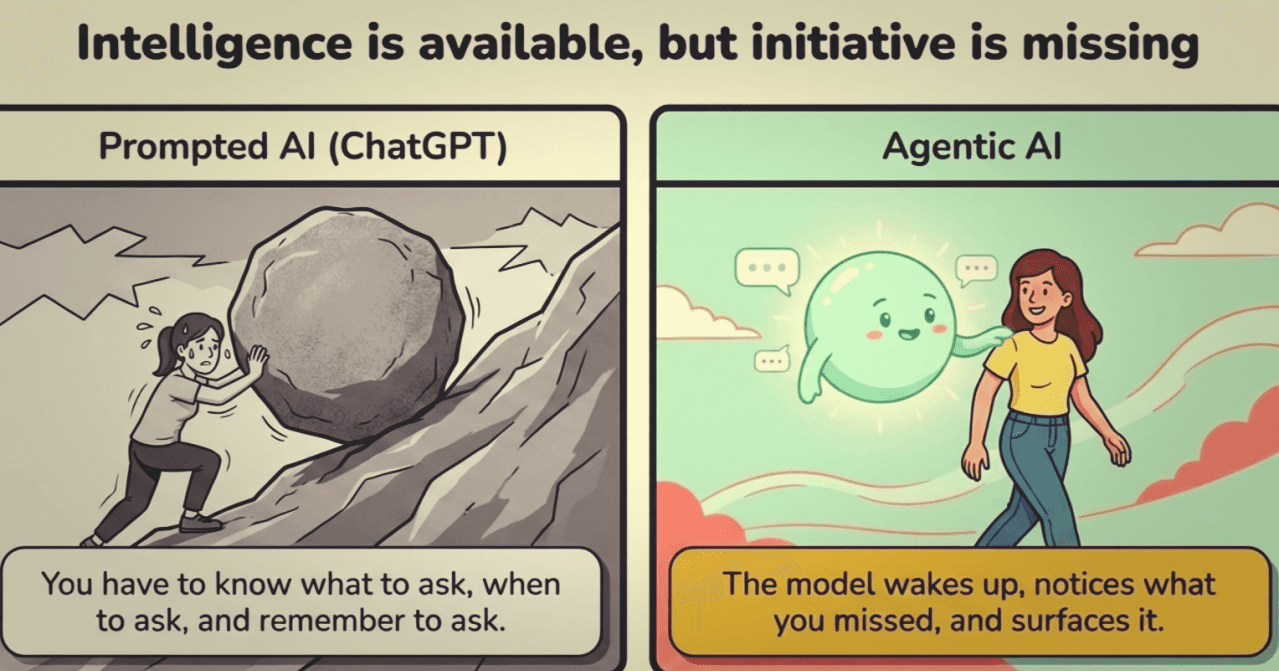

For the last few years, LLMs have put remarkable intelligence in the hands of ordinary users. Ask ChatGPT which mutual fund suits your risk profile and you'll get a more thoughtful answer than most bank websites. That's a genuine step forward.

But it's still you doing the asking. You have to know what question to ask, when to ask it, and remember to ask it at all. The intelligence is available. The initiative isn't.

Agency is what happens when the model stops waiting. When it wakes up, looks at your financial picture, notices something you'd have missed, and surfaces it before you thought to ask. LLMs gave users intelligence on demand. Agentic AI (LLMs in loop accomplishing a task) puts that intelligence to work on your behalf, continuously, in the background, with tools and skills to back it up.

That's the shift. And in personal finance, it changes everything.

What Agency Actually Looks Like

Your FD matures, the money sits in savings earning 3.5%, and weeks pass before you act. An agentic assistant doesn't wait:

"Your ₹5 lakh FD matures in 18 days. Rates have dropped since you locked in. Based on your portfolio and your daughter's college timeline, here's how I'd think about this."

No product pushed. Just the right question, at the right moment, with enough context to be useful.

Or take what happened to equity investors during the West Asia conflict earlier this year. Portfolios dropped sharply. The instinct to sell and move to safety is almost always wrong. But how would an average investor know that? An agent that understands your portfolio and the macro context tells you how to think about it: this is market-wide, your fund's holdings are unchanged, here's what rebalancing would cost you in exit load and tax. Dashboard versus thinking partner.

And that ULIP you've been meaning to review? Upload the policy. An agent that parses the actual IRR buried in the fine print and compares it to what a term insurance plus index fund would have compounded to isn't advising you. It's just doing the math you didn't know to do.

Levels of Agency

This product doesn't try to do everything on day one.

Level 1 is pure intelligence, proactive surfacing, comparison, analysis. The agent builds a picture from whatever you're comfortable sharing: a bank statement, an existing portfolio, your goals. No license required, analysis/summary and not advice.

Level 2 is action, executing the rebalance, moving the maturing FD, switching the insurance. This needs API partnerships and appropriate licenses. It comes after trust is established.

Level 3 is full autonomy within guardrails you define. The agent manages within the boundaries you set, without needing to check in for every decision. That's further away, and probably should be. Trust has to be earned before it can be delegated.

The reason to build this way isn't just regulatory caution. Financial trust is earned slowly. A product that shows its reasoning, one you can verify with a human advisor, is how you earn the right to act. Users share more as they trust more. The agent improves as the data improves. That's the compounding moat.

One more wall this breaks: language. Advances in voice AI and regional language speech-to-text mean this doesn't have to be a text product for English-comfortable urban users. The same agent, the same quality of insight, available in Hindi, Tamil, Telugu, spoken naturally into a phone. The financially underserved user who never had an RM isn't just in Level 2 cities. They're everywhere, and they're reachable now.

The RM who sold my relative a ULIP wasn't malicious. He was optimising for his incentives, the way people do. The system was the problem, where one side of the table always knows more, and always has something to sell.

The most interesting thing AI can do in personal finance isn't automate transactions. It's fix that asymmetry. Put the quality of thinking a conflict-free, financially literate friend would give you, into everyone's pocket.

That's the product worth building.

Join Raghavendra on Peerlist!

Join amazing folks like Raghavendra and thousands of other builders on Peerlist.

0

0

0